Don't Cheer for the Strong Dollar

The strong dollar is creating a sovereign debt crisis and is further accelerating de-Dollarization

First off, my thoughts are prayers are with the people of Florida, Puerto Rico, Mexico, and any part of the Americas affected by Hurricane Ian and Hurricane Orlene.

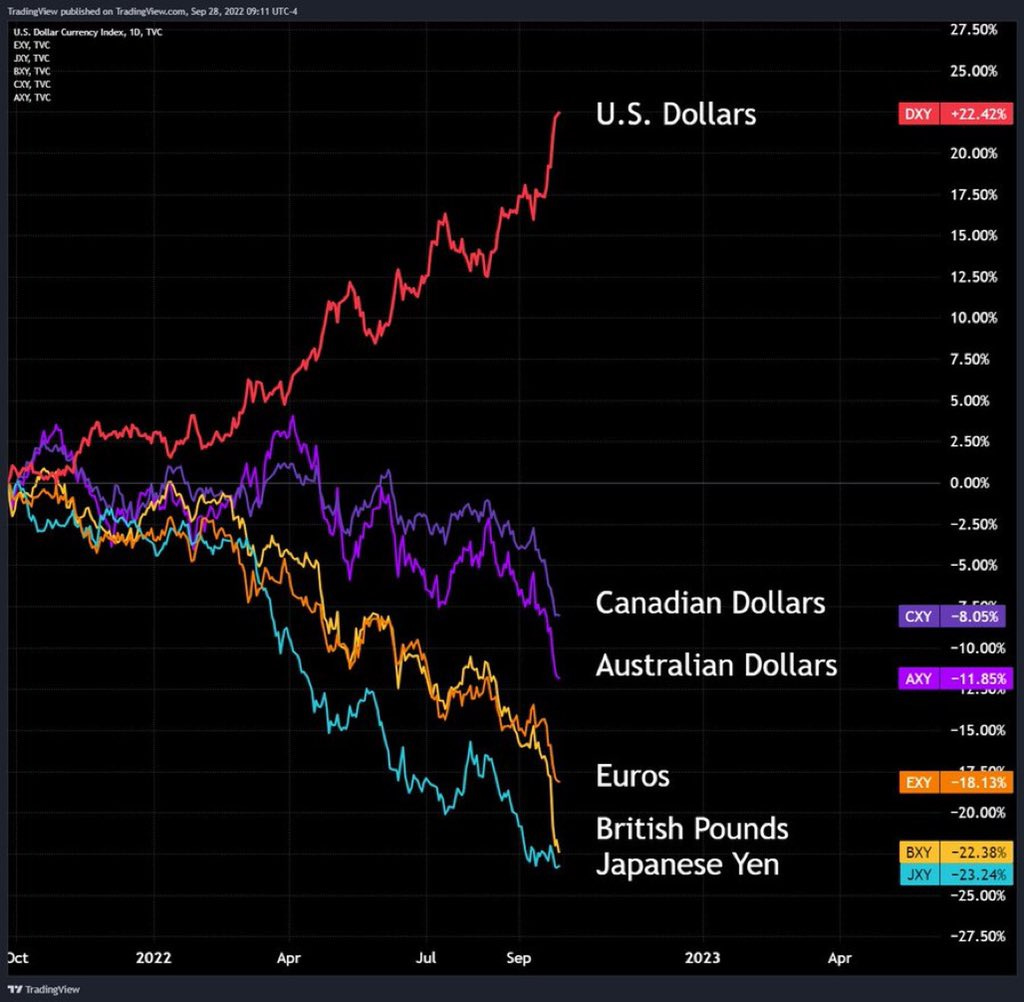

This is the macro chart of the year right here:

As you can see the Dollar is roaring compared to every other global currency. The British Pound and Japanese Yen are down more than 20% compared to the greenback. But is the Dollar actually strong?

Mises.org’s editor and macro analyst Ryan McMaken explains what is really happening with the “strong Dollar”. As he writes below:

Such talk must be heartily opposed, of course, as the dollar is not “too strong,” Rather, talk of the dollar’s “strength” is not really about the dollar at all. It’s about the weakness of other currencies, and it’s about how other central banks have embraced monetary policy that’s even worse than that of the US Fed. If, say, other national governments and central banks are concerned about the dollar being too strong, those institutions are welcome to embrace policies that will strengthen their own currencies.

As he writes above it is not necessarily the fact that the Dollar is strong, but the fact that every other Central Bank globally just had an even more expansive monetary policy. The Bank of England, ECB, and the Bank of Japan have also engaged in money printing and buying their own debt. Real interest rates in Europe and Japan have been in negative territory. Outside of monetary policy, both the EU and Japan are very heavy importers of energy. They both depend on Russia for their energy exports. With banning Russian oil and gas both regions’ economies are suffering and their currencies are on free fall. Also, with interest rates being slightly higher in the US the Dollar has become the “cleanest” dirty shirt of the bunch. For this reason, money has been pouring into the Dollar and Dollar-denominated assets. That is why you are seeing the Dollar shoot up in value compared to other currencies.

The Dollar is strong because every other currency is weak. But let’s look at the Dollar compared to Gold. Gold is a fixed asset (which cannot be printed) and is trusted by Central Banks to be part of their currency reserves. When you look at the 5-year chart below Gold has gone up in value compared to the Dollar, meaning that the Dollar is weaker compared to Gold.

Let’s also look at Bitcoin. As much as people love to gloat about the “decline” of Bitcoin in 5 years Bitcoin has gone up from just $4000 to $19000 now. Also, how can the US Dollar be the strongest currency when the Ruble has been beating every other currency including the Greenback? Western sanctions on Russia have backfired on the West. For anyone who has been reading Armchair Banker this fact is not surprising at all. The Russian Ruble is the strongest currency in the world and has appreciated 45% against the US Dollar as of June. This is all thanks to income from energy exports. So let me ask again, is the Dollar actually strong?

What is next?

As macro legend Luke Gromen has frequently said this year, this is a competition against who has the best balance sheet. To have the best balance sheet a country needs to produce goods and sell these goods into the global market.

As we enter a debt crisis on the sovereign level not seen in close to 40 years countries like the US and UK which heavily propped up the bond market, printed money, and engaged in financialization over 40 years, these economies are seeing immense pain. In the case of the EU (where the ECB was also involved in heavy money printing) and invested less in energy infrastructure are seeing their economy suffer and their currency loses value against the Greenback.

On the other hand countries like China, Russia, and India, have used the past 40 years to build a heavy industrial base, create vast amounts of energy resources, and have found markets to sell these energy exports, and built a real economy. Thus by growing and modernizing their economies all these countries are able to grow massive Forex reserves. Having excess reserves, these countries can afford to take action and fight against a strong Dollar.

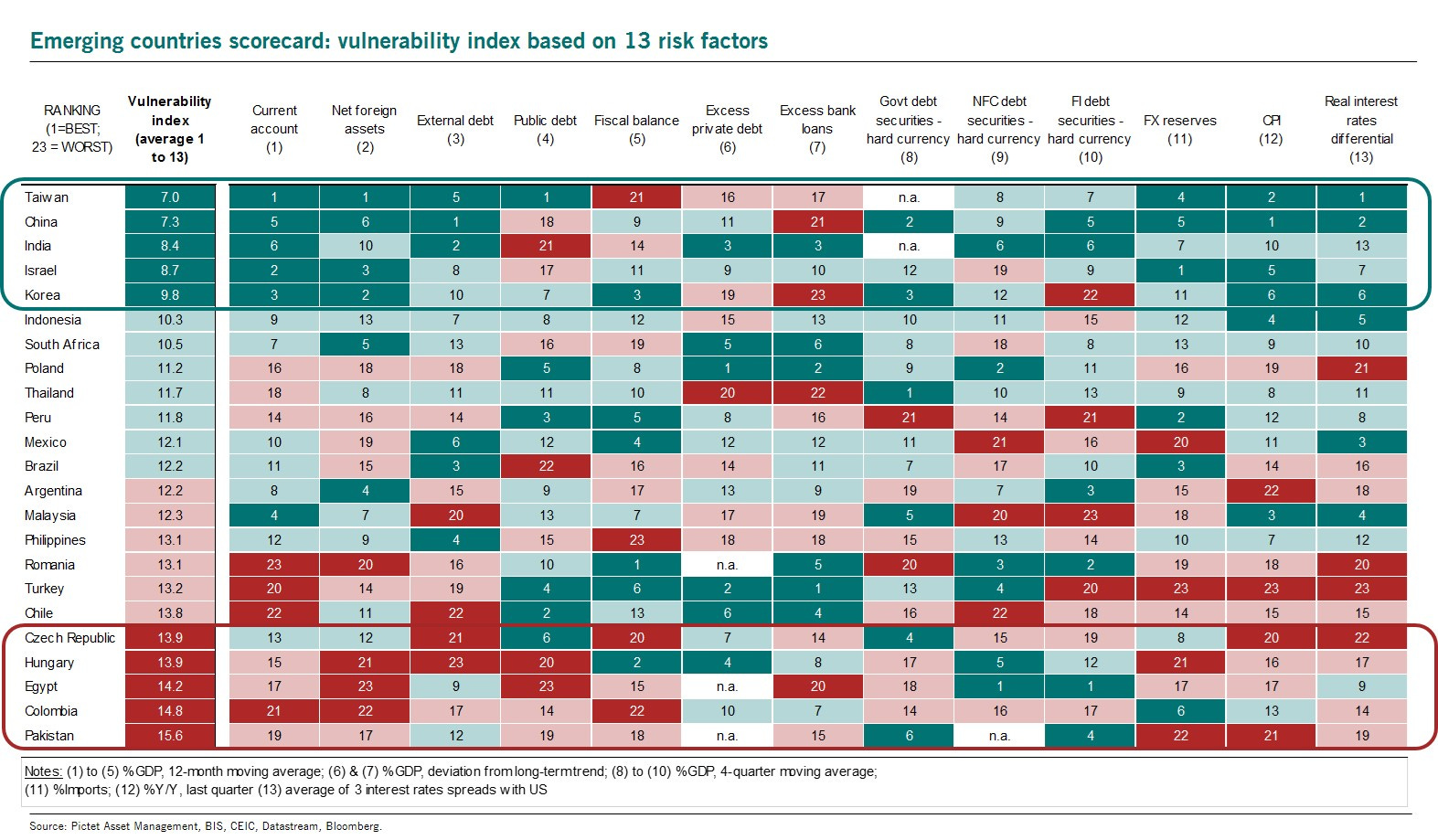

The Chief Economist at Pictet Asset Management Patrick Zweifel tweeted a chart of emerging market countries that are safest from a strong Dollar (shown below):

As you can see above manufacturing hubs like China, Taiwan, and Korea are set to do best during this strong dollar and high inflation period. As the Fed is exporting inflation, countries are switching away from the Dollar.

To maintain China’s mighty economy, the country has had to import its energy. As commodities are priced in Dollars, emerging nations have to sell their forex reserves/print their local currencies to buy Dollars. As the Dollar goes up, countries need to either print more money or sell more of their forex reserves to acquire Dollars to buy commodities. This is one of many reasons for the Sri Lankan economic crisis. This is also a reason why countries want to trade and buy commodities in their local currencies. It is not a secret that China and Russia are de-Dollarizing. But it is not just these two who are ditching the greenback. Even American partners and allies in the region have either already or plan to ditch the Dollar. As we wrote before here on AB Saudi Arabia is already discussing plans to sell oil in Yuan. India has also initiated talks with Saudi Arabia to conduct trade in rupees and Saudi real. India, just like China, is doing realpolitik. India has a 1.38 billion population. India is watching what is happening in Europe and they don’t want people to go dark at night. They are also seeing what is happening to the Euro, Sterling, and Yen and don’t want to see the Rupee devalue. This is why India, even though being part of the anti-China QUAD “alliance” against China, has defied Washington and has gone ahead to use local currencies to buy discounted Russian energy. Even South Korea and Japan, US defense treaty allies, are signing big energy deals with Russia. South Korea and Russia are signing massive cooperation deals on nuclear energy. Japan has already reclaimed its stake in the Sakhalin II oil and gas project. No doubt these transactions are happening in local currencies. As I have written before, Japan is a mercantilist economy. The country is a manufacturing powerhouse. The country cannot survive without cheap energy from Russia. Same with Korea. It makes sense for both these countries to engage in realpolitik and call Moscow to buy energy with their own currencies. Even Southeast Asia is looking to create a non-Dollar payment system to trade with each other. Of course, countries with strong balance sheets can afford to print money and transact with their own currencies. Countries with high deficits, very low income and inbound investment, and bad balance sheets are going to suffer big time. This is what we saw in Sri Lanka during the summer, which is a canary in the coal mine for the sovereign debt crisis of the 2020s. To counter the strong Dollar, it is the survival of the fittest.

The strong Dollar is coming at the worst time for the US. As currencies like the Yuan, Yen, and Euro get cheaper, their exports become more competitive against American exports. This is a time when Washington has come to the realization that it cannot depend on high-tech semiconductors from Taiwan to power the US tech sector and the military-industrial complex. This is why the Biden Administration passed the Chips Act to invest heavily into building high-tech Chip manufacturing right here in the United States. Having a strong Dollar will make US Chips exports more expensive. Also, with a high-interest rate environment, it will be hard for fixed-income investors to invest in debt that will fund new semiconductor foundries in the US.

Now the bond market. Central Bankers were all talk when they said they were going to hike rates and do QT (aggressively buy back government debt) to counter inflation. As I have written previously on AB, I always thought Central Banks will have to cut rates again and go back to QE. Thank you, Bank of England for proving me correct. As the bond market globally has been propped up for 40 years pension funds, mutual funds, and other big institutional investors have been heavy buyers of fixed income securities. This included heavy purchases of government bonds. This was also a time when financialization and financial engineering took over the pension fund system. As reported in the New York Times:

The strategy emerged in the late 1990s and grew in popularity as interest rates tumbled after the 2008 financial crisis. These complex financial instruments are structured so that the party on the other side of the trade would pay the pension fund when bond prices rose, but the pension fund would have to pay the counterparty when bond prices fell.

Pension funds bought financial instruments where as long as the bond prices went up the pension fund got paid, but when prices fell the pension fund was on the hook to pay the counterparty. This is eerily similar to the mortgage crisis where AIG got paid on its credit default swaps as long as housing prices went up and subprime mortgage bonds did not collapse. But when the housing and the mortgage bond market collapsed AIG was on the hook. As bond prices in the UK kept falling to pay its collateral British Pension Funds started selling off UK government bonds. This broke the bond market. Given that Britain still needs to borrow money to cover its expenses, British government bonds need to be investible and “risk-free”. Therefore, the Bank of England had to intervene.

If you think this will not happen in the U.S. you will want to think again. As you can see below most US government debt is owned by the Fed and domestic institutions. If you look closely close to $2 trillion worth of government bonds are owned by pension plans. Do you really think pensioners are going to tolerate their holdings going down? It is also not just fixed income holdings of pensions. Many of these pension holdings have investments in equities. As many young employees have 401k plans, many of these plans have massive holdings of equity funds. The Buffett indicator of stock market cap to GDP is still at an all-time high of 150%. The stock market has still ways to fall. Do you think the Fed can allow a retirement crisis to happen in the U.S.? As they say on FinTwit, you can’t taper a Ponzi.

Also, legendary investor Stan Druckenmiller had a dire warning. Here is what he said:

But if you look at the reversal I just talked about and you use the CBO estimate, which is rates at 3.8 percent, which I think, frankly, is pretty optimistic given all the things we’ve talked about, by 2027, the interest expense alone on the debt eats all health care spending. By 2047, it eats all discretionary spending. So we’re now getting into fiscal dominance. By the way, by ’49, it eats all Social Security. We’re getting to the point now where the interest expense on the debt is so high that it’s going to eat up our ability to basically service the next generation, and I’m not even sure about the current one.

Basically by continuing to raise rates the interest expense of US Government debt is going to eat up most discretionary government spending, which includes social security. Interest expense is the expense on the debt that needs to be paid to US creditors. Do you really think the Fed and US Government will allow pensioners to hungry to serve the US debt? The U.S. has two options, say sorry to either the pensioners or the creditors or just buy back bonds to save the bond market. Knowing this foreign holders of US debt are going to dump Treasury securities. This is where the bond market is at risk of breaking. Already foreign creditors like Japan, China, and even the UK are dumping US Treasuries to stabilize their currencies. As more foreign and even domestic holders dump declining Treasury securities, the Fed will have to come to the rescue. This is where the Fed will pivot.

It is not just treasuries China is planning to dump. The Yuan has fallen against the Dollar. To stabilize the Yuan Chinese Chinese state banks are planning for a massive dump of US Dollars. As we have written before China is the largest trading partner for most countries in the world, especially in the global south. As China wants to speed up its Belt and Road initiative and further pull the global south into China’s sphere of influence, China will engage in trade with these countries in local currencies. It is not just the global south that is engaging in trade with China using Yuan. Australia’s BHP Billiton sold $14.1 million ($100 million Yuan) of Iron ore to China in Chinese Yuan. This is BHP’s first ever sale to China in Yuan. Both Vale (based in Brazil) and BHP have discussed selling to Chinese in Yuan using Blockchain. Maybe an international use case for the Digital Yuan.

Finally, this is what years of kicking the can looks like. After the collapse of the stock market in 2001 rates were cut and the bubble was kicked up to real estate. After 2008 instead of reforming the banking system, re-regulating derivatives and commodities trading, and most importantly bringing manufacturing and supply chains back to the US, Washington just kicked the can. To prop up the Dollar and the bond market, the US just started printing money, artificially reduced rates, and bought every fixed income security from mortgage-backed securities to Treasury bonds. With low-interest rates and Fed intervention of the market bondholders, stockholders, real estate owners, and private equity titans won big from the everything bubble. Foreign Central banks, to compete with the Dollar and the Fed, also started printing money and buying bonds on a massive scale. In the global south, countries like Sri Lanka printed their local currencies and borrowed from Wall Street and the City of London to live beyond their means. Now the party is coming to an end. As we see the everything bubble burst, it is the countries with the strongest balance sheet that can build real things people need and produce energy to build an economy that will win in the end.

What I write here is not investment advice. In this case, these are my macro thoughts. Please do your own research or consult a professional when you are investing. Investing involves risk.

Please share this article on your favorite social media platform. I am new to Substack. Please subscribe to my newsletter. Also, I am still on Medium. Please follow my work on Medium as well.

As always live well, stay healthy, and prosper!!!