OPEC Made the Fed’s Life Much Harder

This could not come at a worse time for Chairman Powell and the US Economy

Courtesy: Seattle Times. Cartoon illustrated by David Horsey.

OPEC has done it again. OPEC+ has agreed to cut oil production by a million barrels a day. Combined with previous cuts, OPEC+’s total oil cuts have come up to 2 million barrels a day. This is 3% of total global oil production. OPEC is already pledging additional production cuts by 500,000 barrels after May of this year. This is bad news for the US consumer and the Fed.

Oil prices have gone up by 6.5%. This is giving pain to the already suffering average American. This is also giving a headache to Fed Chairman Jerome Powell.

The American consumer has been suffering for more than a year from inflation. This February, US CPI went up by 0.4%, to a total CPI of 5.5%. Food inflation alone is 9.5%. Even though mortgage rates are up, home prices are still at an all-time high, which is pushing out first-time home buyers. Already the Fed has broken the US banking system and banks in US and Europe are feeling the brunt. But it looks like the worse is yet to come.

Jerome Powell is not going to stop till inflation comes to an end and the US hits its standard 2% inflation. This has been on the thorn of the side of OPEC. Both the Fed and OPEC have been playing chicken with each other on oil prices. This is a big middle finger to Washington, which is desperately trying to tame inflation while breaking some things in the system.

The current inflation crisis highlights two points. One is that inflation is out of the Fed’s control. The Fed can raise rates but can it drill for oil and grow food? I do not think so. The second point is the ticking debt time bomb.

Fed Chair Jerome Powell is trying to be the next Paul Volker but in reality, it is not going to be easy for him to channel his inner Volker. Back when Volker was Fed chair, the economy was much less financialized and the US debt to GDP was just around 30%. The same cannot be said about today’s leveraged US economy.

Just take US Debt to GDP. The nation’s debt to GDP is 123%. Due to rates going up interest expense on US debt has risen up drastically since the “end” of QE.

But it is not just the national debt. Thanks to deindustrialization and financialization, the whole US economy is levered. This includes corporate debt, commercial real estate, and private debt (private equity and venture capital).

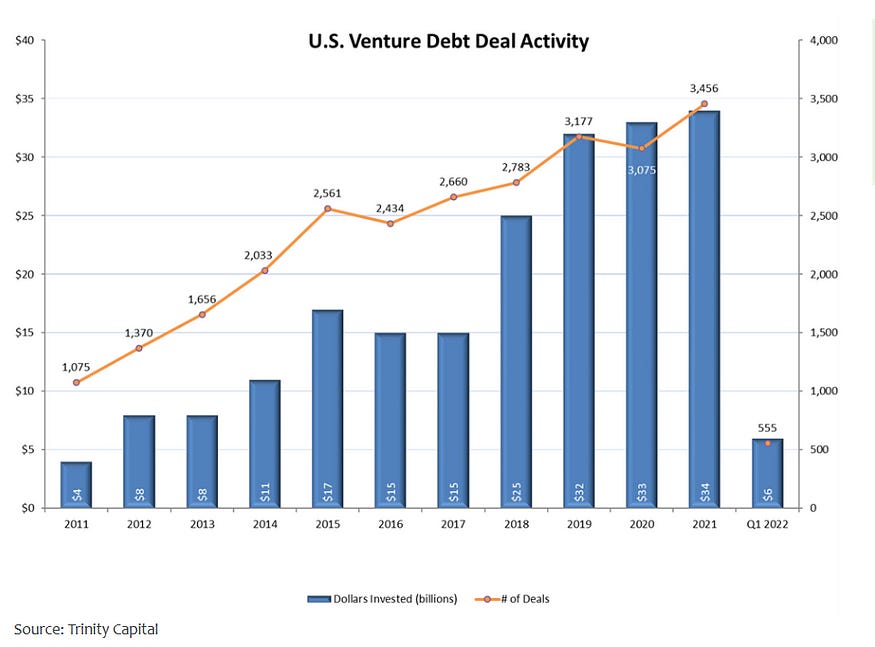

As you can see above corporate debt in the US, including outstanding loans, are at an all-time high. Ultra-low interest rates and the easy money era made it cheap for companies to borrow through capital markets. Many companies used this as an opportunity to boost their earnings per share by borrowing through the open market to buy back shares, thus reducing the number of shares outstanding, which artificially increases the earnings per share (which is Earnings/Shares outstanding). As you can infer from the formula, the fewer shares outstanding means a boost for EPS, which in return props up the stock of publicly traded companies. The easy money era artificially boosted the value of stocks, hence one reason for the overvalued stock market during the 2010s and early 2020s.

Then comes real estate. As yields were at zero, investors desperate for yield went on to invest in real estate. This led to an artificial boom in real estate asset prices. This boom led to demand for commercial real estate construction and investment. Hence, banks, shadow banks, and other institutions started lending to commercial real estate developers and investors. According to Morgan Stanley, $1.5 trillion worth of commercial real estate debt is due to mature by 2025. With interest rates going up and rents and valuations going down, commercial real estate investors are going to have a hard time refinancing their real estate debt. During the late 2010s and early 2020s, increasingly local and regional banks were involved in this lending.

Many borrowers who borrowed using floating-rate mortgages are also starting to feel the pain as rates continue to rise.

Another concern includes commercial property valuations. This is especially a big concern for office real estate. Due to the work-from-home phenomenon thanks to the pandemic, office landlords have been suffering from a cash flow decline thanks to tenants abandoning office leases. Already commercial properties have lost 15% of their valuation. According to Green Street, high-quality office buildings have lost a quarter of their valuation since the pandemic. This decline in property valuations and increasing interest rates are going to make refinancing commercial real estate debt much harder. To add insult to injury, since the Fed raised rates, deposits are leaving banks. As you can see below outflows from banks have skyrocketed. With banks losing deposits, banks will be less likely to lend, which will further hamper the US economy.

Let’s also not forget private debt. As I wrote before, Credit Suisse was a leader in packaging and selling CLOs and selling these types of private debt to institutional investors. Not only CLOs, but during the ZIRP and easy money era overall private debt and lending skyrocketed. Leverage buyout debt grew from around $20 billion in 2008 (right during the GFC) to a whopping $146 billion in 2021.

CLO issuance, which made banks like Credit Suisse very rich, reached $150 billion in 2021. The overall CLO market has reached $1 trillion.

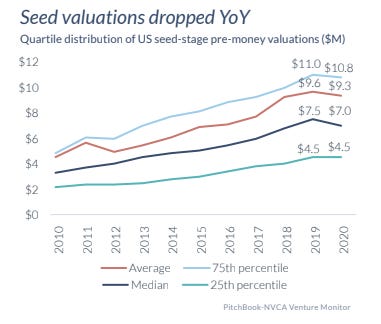

Last but not least is venture debt. Another result of the ZIRP and easy money era was the rise of venture capital. In particular venture debt became popular during the 2010s. This led to the propping up of unprofitable startups and Silicon Valley fraudsters and grifters like Elizabeth Holmes, Sam Bankman-Fried, Tik Tok influencers, and Chamath Palihapitya (not a fraudster but a grifter no less). Let’s also not forget that this era also gave us billionaire crybabies like Bill Ackman and the Tiger Cub hedge funds (Tiger Global, Coatue Management, Lone Pine Capital, etc.).

It is not just venture debt. Venture Capital funded start-up valuations skyrocketed during the 2010s. This subsidized unprofitable tech unicorns like Uber, AirBnB, and DoorDash. This decline in valuations, which led to startups panicking, lead to a bank run that bankrupted the nation’s 16th largest bank.

This brewing debt crisis thanks to the end of ZIRP and easy money era is not just contained to Wall Street. Many commercial real estate lenders for example were local and regional banks in the US. This type of risky lending led to the downfall of Signature Bank in New York. Many of these regional banks, thanks to easy money, started lending to large developers and investors of real estate in major metropolitan areas in the US. For example, Little Rock, Arkansas-based regional bank Bank of the Ozarks (Bank OZK), became one of the largest lenders to real estate developers in Manhattan and Florida. Some major projects financed by the Bank of the Ozarks include:

$410 million loan to Rabina, a developer of a roughly 1,000-foot-tall Manhattan office and luxury residential tower on Fifth Avenue

The bank’s largest deal. $664 million construction loan for a mixed-use development in Tampa Bay, FL backed by Tampa Bay Lightning Owner Jeff Vinick and Bill Gates’ family office

$558 million construction loan in 2018 for a condo project in Sunny Isles, FL

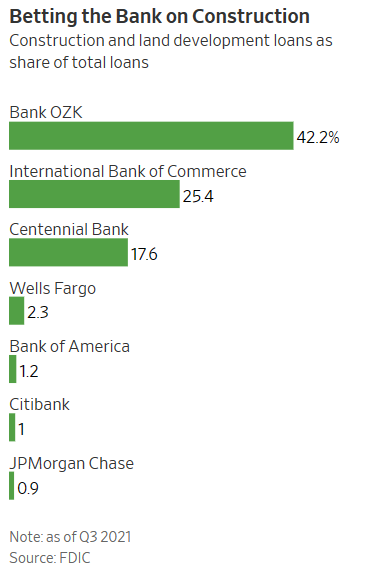

As shown below, Bank OZK’s construction and land development loan book as a percent of its total loans is larger than the biggest money center banks.

As you can see below, smaller banks issued more construction and land development loans compared to their large bank counterparts (like JP Morgan, Bank of America, and Wells Fargo).

It is not just regional banks. Many of these high-risk private debts, like venture debt and CLOs, are held by foundations, endowments, institutions, and pension funds. As I have written before, many pension funds that invested in risk-free securities and safe fixed-income investments were suffering from low returns thanks to ultra-low interest rates. This led pension fund managers to invest in high-risk investments. These include buying packaged debt securities like CMBS and CLOs. Let’s also not forget that many of these investors are major LPs for private equity, venture capital, and hedge funds like Blackstone and Tiger Global. A lot of these pension funds also directly invested in startups, like the Ontario Teacher’s Pension Fund which lost money thanks to investing in FTX. As the bubble pops, no doubt many endowments, foundations, and pensions are painfully seeing their investments go down. But as they say, there is a sucker born every day. Blackstone, which is not letting investors redeem their funds, has already raised more than $30 billion for its Real Estate Partners X fund. Some of its largest investors include the Teachers’ Retirement System of Louisiana, the Arkansas Teacher Retirement System, the Oklahoma Teachers’ Retirement System, the Tennessee Consolidated Retirement System, the Minnesota State Board of Investment, the Teachers’ Retirement System of the State of Illinois, and the New York State Common Retirement Fund. This is happening as pressure is mounting against commercial property valuations and CMBS debt prices.

In conclusion, Powell would love to be Volker. But Volker was Fed chairman at a time when the US economy was still a manufacturing and trading powerhouse, far less financialized and levered, and the US debt/GDP was around 30%. Yes, Volker broke some things but in the end, beat inflation and helped the US economy get back to growth and prosperity during the 80s and 90s. But the US has much more debt. By raising rates, its interest payments are skyrocketing. Also, unlike in the 1970s, the US economy is much more financialized where building real things and exporting goods have been replaced by financial engineering and speculation. As I have written above, this has led to an over-levered economy. This leverage also includes increased household, student loan, and credit card debt. I have also highlighted previously how asset bubbles are needed to bring in tax revenue for US local, state, and federal governments. We have already seen how a few basis point rate hikes have taken down 5 banks in the US. As the US economy is much more levered, more rate hikes mean more things are about to break. It does not help that OPEC (led by Saudi Arabia) has cut oil production. These cuts are coming at a time when CPI in the US is slowly coming down. But these cuts show that the Fed still has a long way to go when it comes to fighting inflation and bringing inflation down to the normal 2%. OPEC+’ moves may force Powell to raise rates even more, which will continue to break Wall Street’s paper empire and take down the US economy with it.

None of this is investment advice. Please follow me here and on Medium. Live well, stay healthy, and prosper!!!