Outpacing America: How China is Winning the AI Race

A few points may suggest that China is gaining the upper hand in the global AI race

AI is always on the news. Mainstream financial media cannot get enough of AI. We here in Macro Essays have frequently spoken about AI but in a contrarian view rarely heard on mainstream financial media. This is another one of those view you won’t see anywhere.

Mainstream media, especially in the US, is captivated by discussions of AI, the Mag7, and NVIDIA. There’s an almost obsessive focus on NVIDIA, with constant speculation about when the company’s market cap will hit $4 trillion!! However, the reality of AI is far harsher than what anyone in the media, Washington, or Silicon Valley is willing to admit.

First, let’s look at the sheer numbers. If you look at the sheer numbers below, China graduated more STEM graduates than the US and EU combined!!!! (courtesy: Georgetown CSET)

This is not just on the undergraduate level. By 2025, China is to double the US number of STEM PHDs (Courtesy: CSET).

Not only this is showing in sheer numbers, but is showing in global university rankings. Not only China has grabbed 6 out of the top 10 global university rankings, But China has releleased more AI research papers than the US and EU (Courtesy: Bertelsmann Foundation).

Many in the West love to talk about how the West, especially the US, has a strong working-class population and how demographics is an advantage compared to China. But China boasts a much larger younger population competent and have the skills needed to take on the 4th Industrial Revolution.

I will finish this point by linking to this article on MacroPolo. Majority of AI talent in US grad schools come from China and many of them stay and work in the US. Now with the increased tensions between the two superpowers, imagine if these Chinese talent start migrating back home?

In addition to its vast pool of talent in science, math, and engineering, China also has greater access to energy. Unlike the previous technological revolutions—such as the personal computer and internet innovation—this one is likely to be inflationary. Wall Street has already expressed concerns about the cost of infrastructure and the high energy consumption involved. For instance, according to the International Energy Agency (IEA), data center energy usage is expected to double by 2026, reaching 1,000 terawatt-hours—equivalent to Japan's total electricity consumption. This is another area where China is outpacing the United States.

As I’ve previously discussed, the electrification of the world—through EVs, green technology, and AI—combined with the rising middle class in the Global South, will demand a significant amount of energy. For China to achieve its green energy ambitions, advance high-tech innovation, and serve its ever-growing middle class, cheap energy is essential, and China is well aware of this. As the chart below illustrates, for China to become a wealthy nation and escape the middle-income trap, access to affordable energy is crucial.

Courtesy: Tracy Schuchart Twitter

For China, there are two key strategies: increasing the use of the Yuan in global trade and expanding nuclear and solar energy production. By boosting Yuan-based trade, China can effectively print its way to securing cheap energy, rather than depleting its US Dollar reserves. To this end, China has been signing currency swap agreements with major commodity providers, including Saudi Arabia. These swaps enable China to collaborate with fossil fuel and commodity producers in countries eager to align more closely with China. Additionally, with Western nations shunning Russia after 2022, China can easily access cheaper energy from its northern neighbor.

Second, China is the global leader in nuclear energy. If you’ve been following Macro Essays, it’s no surprise that we are very bullish on nuclear energy. Many nations have recognized that nuclear power is the cheapest, safest, and least CO2-intensive energy source available. China has fully embraced this reality, rapidly expanding its nuclear energy infrastructure. As shown below, China leads the world in the construction of nuclear reactors and the growth of net electrical capacity through nuclear energy.

Thanks to increased investment in nuclear and solar energy, along with easy access to commodities in an increasingly Eastern-oriented global economy, the price of electricity in China is significantly lower than in the United States. As of March 2023, the cost of electricity per kilowatt-hour in China is 8 cents, compared to 18 cents in the US. AI innovation thrives on cheap, reliable electricity, and China is excelling in this area. By continuing to advance in nuclear energy, China is aiming for energy self-sufficiency, the eradication of greenhouse gas emissions, and affordable energy access for its billions of citizens.

The competition in AI innovation is largely about who can access the cheapest electricity. Affordable electricity translates directly into greater computing power for AI development. In this regard, China not only leads in nuclear technology innovation but also enjoys much lower electricity costs compared to the West. By heavily investing in cost-effective energy sources and leveraging Western sanctions on Russia, China has secured access to cheap electricity, often using its own currency. This advantage will significantly boost China's computing and innovation capabilities in AI.

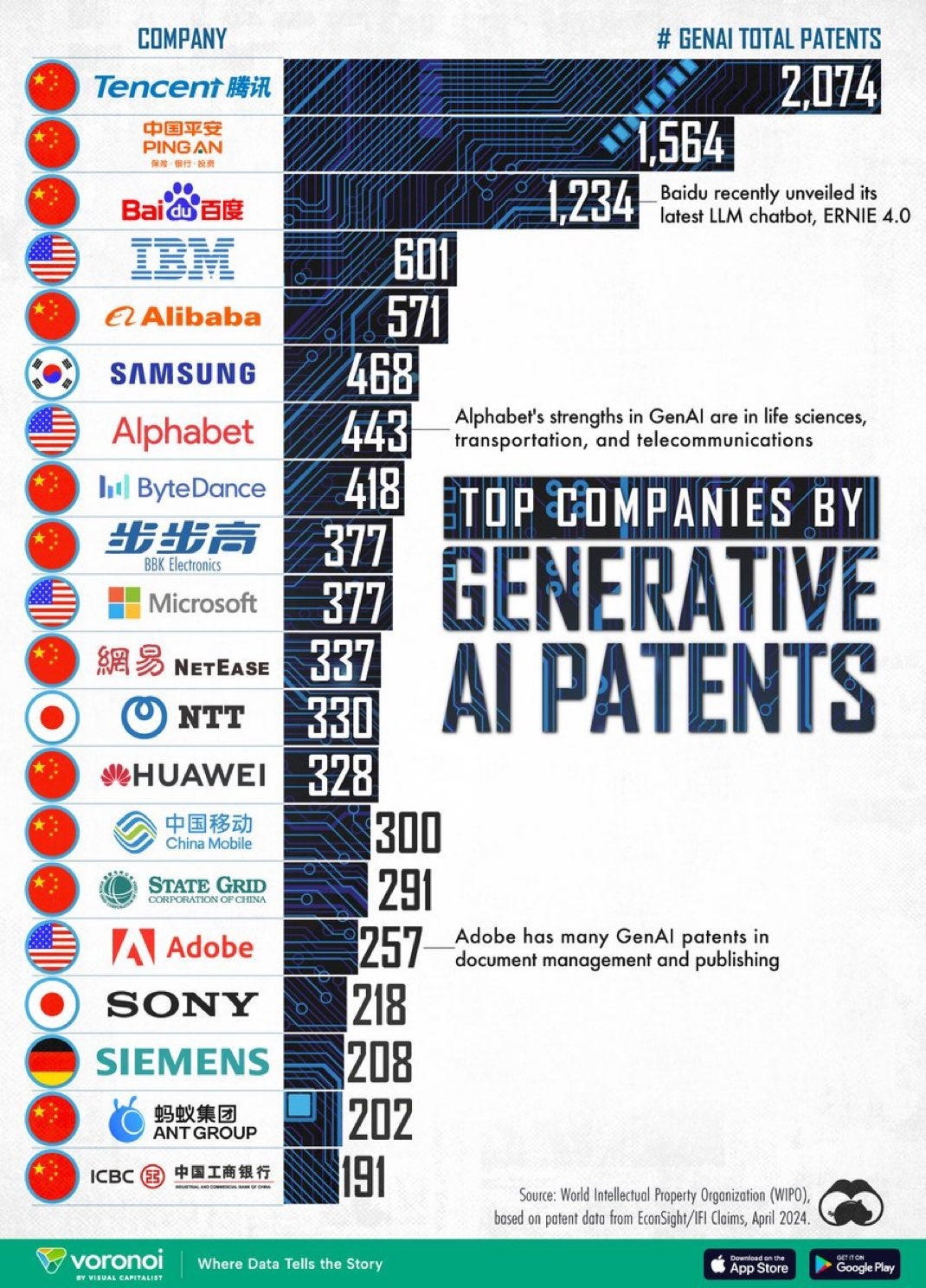

When you analyse all of this, the chart below makes sense (courtesy: Dan Collins’ Twitter).

As you can see above, China is dominating the generative AI patent race. Notably, aside from Siemens, there isn’t a single European company on the chart. With the EU heading toward an energy crisis, Europe is poised to be the true loser in the AI race—compounding the setback from missing out on the Web 2.0 revolution. The loss of access to cheap Russian energy is likely to undermine Europe’s chances of being a leader in this century.

Third, China can borrow cheaply and build infrastructure much faster than any Western nation.

As you can see above, long-term rates on Chinese government bonds are much lower than those on US government bonds. This allows Beijing to issue more debt at a lower cost compared to Washington, which helps stimulate its economy. Beyond rates, China’s infrastructure development is both fast and efficient. Videos of China’s cyberpunk cities, like Shenzhen, Shanghai, Beijing, and Chongqing, showcase their transformation from modest beginnings to bustling mega-metropolises that appear as if they belong to the year 2100.

Building infrastructure, manufacturing, factories, and logistics are China's specialties. Chinese technology leaders are highly confident in the country’s ability to develop infrastructure. For instance, Henry He, Executive Director and CFO of Kingsoft Cloud, has praised China’s advancements in computing infrastructure, noting improvements over the past 2-3 years. This infrastructure includes constructing vast data centers and maintaining a power grid robust enough to support AI. With China having a low inflation rate (and facing deflation) compared to the US, it will be convenient for the middle kingdom to build up infrastructure, computing power, and energy infrastructure needed to power the Fourth Industrial Revolution.

According to Wells Fargo, electricity consumption due to AI is expected to increase from 8 TWh to 52 TWh by 2026, marking a 550% rise. By 2030, electricity usage is predicted to soar to 652 TWh, a staggering 1150% increase. Many in the US are concerned about the electrical grid's ability to handle such growing energy demands from emerging technologies. For example, California is already grappling with power grid issues related to EVs. Introducing AI could add even more strain. Imagine the impact if Silicon Valley companies begin heavily investing in AI—how much additional pressure would it place on California’s electrical grid?

This is why China is heavily investing in green energy technologies, ranging from solar to nuclear power. China leads the world in solar panel manufacturing and has 40 nuclear power plants in operation, while the US has only one under construction. Not only does China have easy access to energy, but it also possesses the infrastructure needed to support the AI boom.

Finally, consider this chart: in 1993, the US had the ability to generate four times more electricity than China. Fast forward to 2023, and China's electricity generation capacity is now twice that of the US. This significant shift provides China with a major advantage over the US.

Image Courtesy: SL Kanthan’s Twitter

Third, unlike the internet—particularly Web 2.0—smartphone applications, and software, AI demands substantial capital expenditures (CAPEX). Prominent investment firms like Goldman Sachs, Barclays, and the renowned venture capital firm Sequoia have questioned whether large tech firms can achieve solid returns on the significant investments required. Sequoia’s memo, authored by David Cahn, an investor and talented tech analyst at the firm, raises a crucial question about the increasing CAPEX by tech companies and their less-than-stellar results. Cahn specifically inquires how Silicon Valley’s major tech firms plan to address the '125B hole that needs to be filled for each year of CAPEX at today’s levels.'

The rise of Silicon Valley in the 2010s was driven by a low-interest-rate environment. Publicly traded giants like Google and Meta were able to grow their earnings per share by borrowing at low rates and buying back stock to boost share prices. This influx of cash led Silicon Valley VCs to invest heavily in low CAPEX businesses like SaaS companies and cash-burning tech unicorns. Wall Street investors favored these FAANG stocks because they required minimal CAPEX and were asset-light.

During this period, the US economy became increasingly financialized, and supply chains were outsourced to Asia. However, the AI revolution is different. While the 2010 tech boom was characterized by easy money flowing into Silicon Valley, inflated valuations from cash-flush VCs, and minimal concern for CAPEX to appease Wall Street, the AI revolution will involve massive investments in science and technology talent, infrastructure, and manufacturing capabilities, particularly in semiconductors. According to a report from the Washington, D.C.-based Center for Economic and Policy Research, China stands as the global manufacturing superpower.

In terms of manufacturing, we’re not just talking about producing plastics or everyday items like socks and shoes. China is a global superpower in high-tech exports, including electronics, metals, and chemicals. This dominance is a major concern for Washington, which is why the CHIPS Act was created.

Even with the CHIPS Act, the US faces significant challenges in regaining its manufacturing foothold. TSMC has raised concerns about the difficulties it encounters with its expansion in Arizona, including issues with infrastructure and the challenge of finding skilled talent for semiconductor manufacturing in the US (see my previous piece on semiconductors).

Finally, here is another chart of global high-tech exports by countries (source: SL Kanthan Twitter):

Finally, and most importantly, China's need and urgency to build and develop AI is much greater than that of the US. Let me explain. For China, demographics present a challenge that AI is poised to address. Contrary to the concerns of many China skeptics, the demographic issue is not as pressing for Beijing as it might seem. As mentioned earlier, China already outperforms the West in terms of STEM talent among its youth. The main issue Beijing is tackling is the replacement of low-skilled factory workers. When China opened up and joined the WTO in 2001, it became a hotspot for multinationals seeking cheap labor. However, as China advances up the manufacturing value chain and its middle class grows, many young Chinese are unwilling to work in low-wage factory jobs, highlighting the true demographic challenge (courtesy: Statista).

In contrast, the situation in the US is quite different. The majority of US GDP comes from services and private industry, totaling a staggering $23.5 trillion. Much of the discussion about AI in the US revolves around its potential to replace roles in these service sectors. This isn't limited to mundane jobs; it extends to high-profile positions such as investment bankers, hedge fund managers, real estate brokers, doctors, and lawyers—some of the largest taxpayers and key voting blocks. The question arises: will US politicians allow AI to advance unchecked if it threatens to displace these influential professionals? The risk of significant pushback from those seeking to protect their jobs could influence policy decisions.

For years, Wall Street and media outlets like CNBC have glamorized AI, but recently, they have begun to question its viability. The primary concern is the substantial capital expenditures (CapEx) required by tech firms, which are yielding minimal returns. Given an economic and financial system that prioritizes short-term gains, money printing, and extreme financial engineering, there’s skepticism about whether long-term AI success is feasible—especially when competing against a long-term-focused industrial powerhouse like China.

That said, the US is not without its advantages compared to China. The US still boasts some of the largest market-cap tech firms, the world’s leading STEM research universities, and a strong pool of tech talent eager to come to the US. However, in the grand scheme of things, the current edge belongs to China. To compete effectively in the 21st-century AI race, the US will need to make a concerted and significant effort.

If the previous technology revolution brought sky-high stock market returns, deflation, and a significant productivity boost, this new technological revolution will demand much more energy, extensive infrastructure development, and may lead to inflation and social unrest. The country that excels in tech talent, cheap electricity, access to commodities, and manufacturing capabilities will likely dominate the global AI race. As it stands, China is currently ahead.

None of this should be considered investment advice. Please consult a professional before making any investment decisions. I write these analyses for educational and entertainment purposes. If you enjoy this type of analysis, please follow me on Substack and Medium. All of my research is free, but additional funds for news sources and analytics tools would enable me to provide even more comprehensive and detailed analysis to support your investment decisions. Please consider supporting me by subscribing to my annual newsletter as a form of donation. As always, live well, stay healthy, and prosper!!!